Yes, you can own a home after bankruptcy. Lenders care about time since the event, how you’ve managed credit since, and the type of loan you’re applying for. Below is exactly how to get mortgage-ready after Chapter 7 or Chapter 13, with realistic timelines and lender expectations.

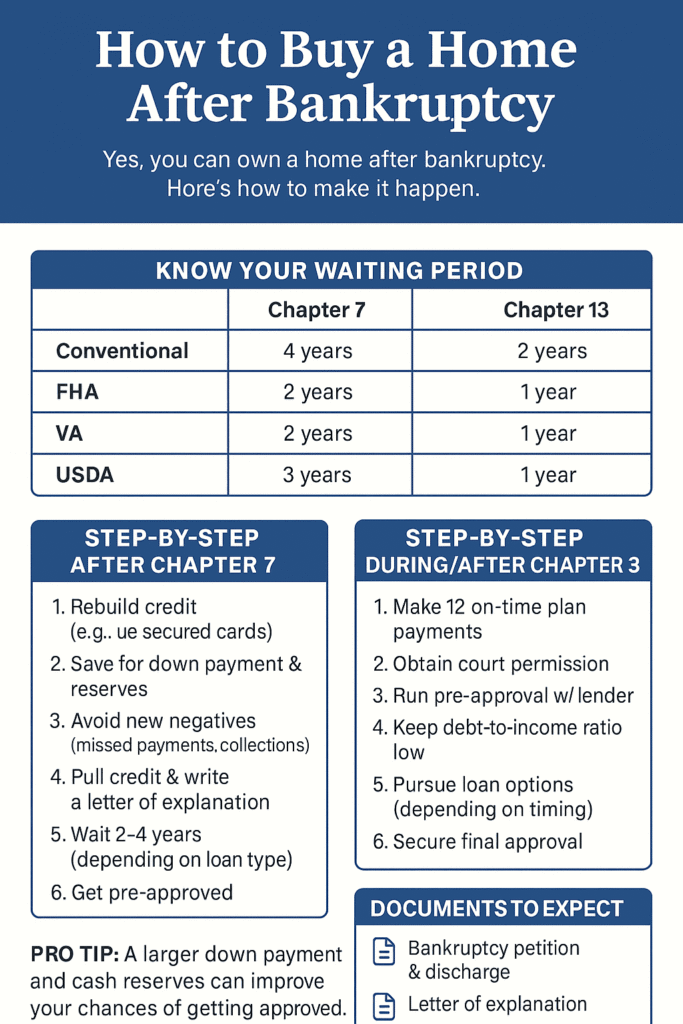

Know Your Waiting Periods (By Loan Type)

Conventional (Fannie Mae/Freddie Mac)

- Chapter 7: Wait 4 years from discharge/dismissal (can be 2 years with documented extenuating circumstances).

- Chapter 13: 2 years from discharge, 4 years from dismissal (can be 2 years from dismissal with extenuating circumstances).

FHA

- Chapter 7: Generally 2 years from discharge; as little as 12 months with strong extenuating circumstances and re-established credit.

- Chapter 13: Eligible after 12 months of on-time plan payments with court approval; discharge not required.

VA (for eligible Veterans/servicemembers)

- VA sets no hard minimum credit score; lenders set overlays.

- Typical lender practice: ~2 years after Chapter 7 discharge; as soon as 12 months into Chapter 13 with on-time payments and court approval.

USDA (rural homes)

- Chapter 7: After 36 months, it’s not considered adverse credit.

- Chapter 13: If the plan is active and the automated system gives an “Accept,” lenders confirm payments; when the plan’s been completed for 12 months, no extra steps are needed.

⚠️ Lenders can add their own overlays (higher credit score, reserves, etc.). Always verify with a local lender before you shop.

Step-by-Step After

Chapter 7

(Fresh Start)

- Mark your discharge date (your waiting clock starts here).

- Rebuild tradelines (months 1–12):

- Open 1–2 secured cards; keep utilization <10%.

- Add an installment tradeline (credit-builder loan).

- Eliminate new negatives: no late payments, no collections.

- Save for down payment + 2–3 months reserves.

- Month 12–18: Pull credit, dispute errors, and write a concise Letter of Explanation (why BK happened, why it won’t recur).

- Choose your lane:

- FHA if you’re closest to the 2-year mark or qualify under the 12-month extenuating pathway.

- Conventional if you can wait 4 years (or 2 with extenuating).

- Pre-approval & documentation: 2 years of W-2s/1099s, 60 days of assets, BK discharge papers, LOE.

- Shop homes within payment comfort, not max approval.

Step-by-Step During/After

Chapter 13

(Repayment Plan)

- Hit 12 on-time payments in your plan.

- Get written court/trustee permission to incur a new mortgage.

- Ask a lender to run pre-approval (FHA/VA/USDA are common here).

- Keep DTI tight (avoid new debt; season your down payment funds).

- If you’re discharged: you can pursue Conventional after 2 years from discharge (or 4 years from dismissal).

- If plan still active: FHA/VA/USDA may work with court permission and on-time payments per program rules.

Two Real-World Examples

Example A — Chapter 7 → FHA (Fastest Return)

- BK Discharged: March 2024

- You today: Solid 12-month spotless history, two active tradelines, 620+ FICO, 3.5% down

- Path: Target FHA at March 2026 (2-year mark). If you can document extenuating circumstances, some lenders may consider as early as March 2025.

Example B — Chapter 13 → Conventional (Stronger Pricing

- BK Filed: July 2022; Discharged: September 2024

- You today: All plan payments on time, strong income, 680 FICO

- Path: Conventional is eligible after September 2026 (2 years post-discharge). FHA/VA/USDA could be options sooner with court permission if you hadn’t been discharged yet.

Documents Lenders Will Ask For

- Bankruptcy petition & discharge (or Chapter 13 plan + court permission letter).

- Letter of Explanation for the BK (brief, factual).

- 24 months income (W-2/1099/tax returns), recent pay stubs, 60 days bank statements.

- Proof of re-established credit and no new derogatories (Fannie & FHA both expect this).

Credit & Cash: What Helps You Qualify

- Clean 12–24 months of on-time payments (rent matters a lot).

- Low utilization (<10%) and 2–3 open tradelines.

- Reserves (1–3 months) even if not required—strong compensating factor.

- Down payment source: your own funds or allowable gifts per program.

- Know program credit norms:

- Conventional: many lenders look for 620+.

- FHA: 3.5% down typically needs 580+ (10% down if 500–579).

- VA: no VA-set minimum, but many lenders use ~620 overlays.

FAQ (Short & Useful)

Can I buy a home while I’m still in Chapter 13?

Yes—after 12 months of on-time plan payments and with court approval (often FHA/VA/USDA first).

Do “extenuating circumstances” shorten waits?

Sometimes. Conventional can drop from 4 → 2 years (Ch.7) or 4 → 2 years (Ch.13 dismissal) with well-documented, one-time events beyond your control. FHA may allow 12 months (vs. 24) after Ch.7 in narrow cases.

What if I’m in a rural area?

USDA is powerful: Ch.7 older than 36 months isn’t adverse; active/finished Ch.13 can be workable depending on AUS findings and timing.

Quick Compliance Note

This article is for general education, not legal or financial advice. Underwriting rules can change and lenders may add overlays—always confirm your exact path with a qualified lender and (if needed) a bankruptcy attorney.